Does transparency bring cleanliness? Offshore financial secrecy reform and corruption control

The project examined whether international transparency reforms have reduced the use of offshore jurisdictions for hiding corrupt wealth. Using new financial secrecy indicators and leaked data, it traced how shell companies are used to move illicit funds across borders.

To learn more about this project, contact Principal Investigator Daniel Haberly.

Tracing the Impact of Offshore Secrecy Reforms

This project investigated whether global transparency efforts have curbed the use of offshore jurisdictions to conceal illicit wealth—using leaked data and the first historical dataset by jurisdiction on financial secrecy.

Transnational financial networks have long enabled large-scale (‘grand’) corruption, with offshore secrecy jurisdictions—commonly referred to as tax havens—facilitating the movement and concealment of illicit funds tied to corruption, tax evasion, smuggling, and organised crime.

While international reforms have sought to increase financial transparency and curb these practices, there has been limited evidence on whether these efforts have reduced the use of offshore structures for illicit purposes.

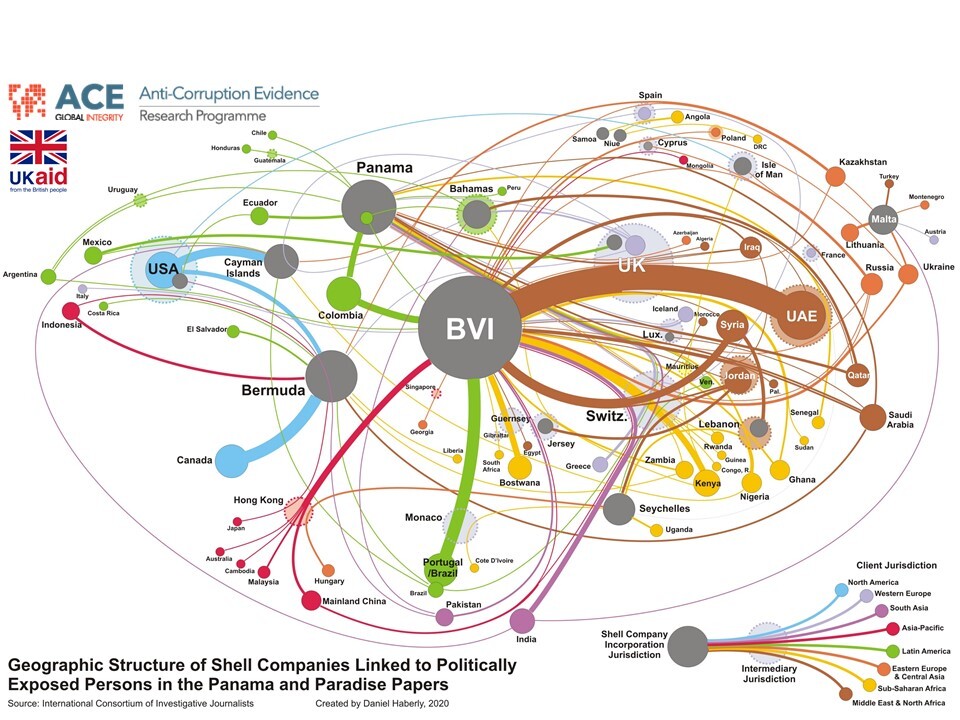

This project addressed that gap by compiling the first historical, jurisdiction-level database of financial secrecy indicators. It used this new dataset to assess how changes in offshore secrecy affected the use of shell companies to hide and move corruption proceeds—drawing on leaked datasets such as the Panama and Paradise Papers.

Key Findings

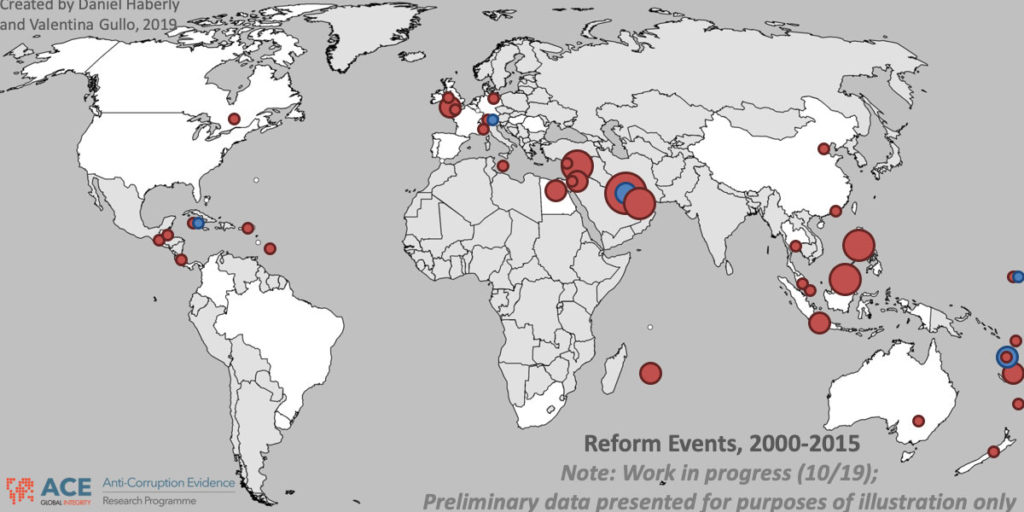

∙ In countries with high levels of political corruption, the formation of offshore shell companies followed predictable patterns. Activity increased during periods of regime stability and was further amplified by economic liberalisation – suggesting greater opportunities for illicit enrichment.

∙ In many cases, governance reforms bundled efforts to strengthen the rule of law with liberalisation measures. The research found that these two objectives should be decoupled, with priority given to rule of law in politically corrupt contexts to avoid unintended risks.

∙ The formation of shell companies in developing and transition economies was not driven solely by elite corruption. Instead, broader macroeconomic trends – such as foreign aid inflows and mineral rents – were also linked to offshore activity. These patterns point to structural vulnerabilities that extend beyond individual misconduct.

∙ The project used the newly developed Regulation of Illicit Financial Flows (RIFF) dataset to provide a consistent, 30-year global view of anti-money laundering (AML), counter-terrorism financing (CTF), and financial secrecy reforms.

∙ While there was clear evidence of regulatory convergence in areas like AML/CTF compliance and international information exchange, major gaps remained – particularly around banking secrecy and beneficial ownership transparency. These weaknesses were found not only in offshore jurisdictions but also among key OECD countries.

∙ Persistent shortcomings in transparency continue to hinder investigations by civil society organisations, journalists, and other non-governmental actors who play a critical role in holding power to account.

Impact and Implications

At a time when reforms around information exchange and beneficial ownership transparency were central to global efforts to combat illicit financial flows, this project provided much-needed quantitative evidence on the effectiveness of those measures. By systematically assessing how reforms influenced the use of offshore shell companies to hide corruption proceeds, the research offered critical insights to inform the design and implementation of future financial transparency initiatives.

Evidence & Impact:

The research was presented at key international forums, including the European Anti-Money Laundering Policy Forum, the International Monetary Fund (IMF), and the Central Bank of The Bahamas Empirical AML Conference – bringing together experts from government intelligence units and financial oversight bodies.

The team engaged directly with stakeholders at the OECD and the European Parliament, contributing to high-level discussions on transparency reform.

As part of broader policy engagement, the project contributed to the UNCTAD–UNODC Task Force on the statistical measurement of illicit financial flows, which aimed to develop a new SDG indicator. It also informed the development of the UK’s proposed International Centre of Excellence on Illicit Finance.

The RIFF dataset produced by the project was used by the United Nations Economic and Social Commission for West Asia in analysing illicit financial flows across the MENA region.

In the UK, the team provided evidence at an Open Ownership event on financial secrecy in the UK and its overseas territories, and contributed to discussions on sanctions, illicit finance, and organised crime at the Changing Geopolitical Order conference, co-sponsored by SOC ACE and GI ACE.

Publications

The Regulation of Illicit Financial Flows (RIFF) Dataset: A New World Map of 30-years of Financial Secrecy and Anti-Money Laundering Reforms

To assess the effectiveness of international efforts to combat illicit financial flows (IFFs), we need a map of how and when specific reforms have been implemented in key jurisdictions around the world over the past few decades.

From Secrecy to Scrutiny: A New Map of Illicit Global Financial Networks and Regulation

This publication focuses on groundbreaking research revealing significant shifts in the pattern of global illicit financial flows (IFFs). The study, led by Dr. Daniel Haberly, reveals how and where different types of illicit money flows around the world.

Corruption, Shell Companies, and Financial Secrecy: Providing an Evidence Base for Anti-Corruption Policy

This paper summarises research exploring patterns of global shell company formation and regulations governing offshore financial secrecy. The research uses big data analytics both to examine existing assumptions held by campaigners, practitioners and policy-makers, and to provide an evidence base…

Sticky Power: Global Financial Networks in the World Economy

Daniel Haberly and Dariusz Wójcik offer a novel theoretical framework for understanding financial networks, which is richly illustrated with data, figures, and visualisations and argues for a new way of thinking about money, finance, and their implications for the world…

Dirty money pushed, dirty money pulled. A gravity analysis of anomalous financial statistics

Literature using gravity specifications to investigate dirty money flows see several limitations both because of the lack of a solid theoretical underpinnings and reliable data. The goal is to develop a method to pinpoint origin-destination (country) pairs that may present…

Related Blogs

Research Team

Daniel Haberly

Principal Investigator

Associate Professor,

Senior Lecturer in Human Geography, University of Sussex School of Global Studies, Centre for the Study of Corruption and Centre for Global Political Economy

Alex Cobham

Chief Executive, Tax Justice Network, and Visiting Fellow, Kings College London

Valentina Gullo

Research Fellow, University of Sussex School of Global Studies and Centre for the Study of Corruption